Content insurance for storage is a dedicated policy designed to protect the financial value of your belongings from disasters like fire, flood, or theft while they’re tucked away in a self storage unit. Think of it as a vital safety net, because the storage facility's own insurance almost never covers your personal or business items.

Why Your Stored Items Need a Safety Net

It’s a common assumption: renting a space at a secure facility automatically means your belongings are protected. But while a facility provides crucial physical security like CCTV and controlled access, this isn't the same as financial protection for your goods.

Imagine it like a secure car park. The security guards are there to deter theft, but they won’t pay to replace your car if a tree falls on it. This is a massive misconception that can lead to heartbreaking financial loss. The storage company’s insurance covers their building and their own liability—not the value of the things you place inside your private unit.

If an unforeseen disaster like a fire or a burst pipe were to happen, you’d be left to cover the replacement costs yourself without a personal policy.

The Real Risks to Your Belongings

It’s absolutely essential to understand the difference between facility security and personal contents cover. The padlock on your unit door is your first line of defence, but it offers zero protection against wider threats. These can include:

- Fire Damage: A fire starting in a neighbouring unit could easily spread, destroying your possessions in minutes.

- Water Damage: A leaking roof or a burst internal pipe can ruin everything, from priceless family photos to expensive electronics.

- Theft: Even the most secure facilities aren't impenetrable. A determined thief could still gain access, making insurance a crucial fallback.

- Vandalism: Malicious damage can render your items completely worthless.

Protecting Your Valuables Is Your Responsibility

Ultimately, the responsibility for insuring the contents of your storage unit rests with you. It doesn't matter if you're storing household furniture during a move, valuable business inventory, or sentimental family heirlooms—their financial value needs its own dedicated protection.

A secure storage unit protects your items from unauthorised access, but content insurance for storage protects their financial worth from unexpected disasters. It transforms your storage solution from a simple space into a fully secured asset.

Choosing the right facility is the first step. You can easily find secure storage near you to ensure your items are physically protected. But the final, critical step is pairing that physical security with a robust insurance policy. It's what gives you complete peace of mind, knowing your assets are financially covered no matter what happens.

Choosing Your Storage Insurance Path

When it comes to insuring your stuff in storage, you’ve basically got two main paths to choose from. Which one is right for you will boil down to a mix of convenience, cost, and just how much cover your belongings really need. Let's break them down so you can make a smart decision.

Your first option, and often the simplest, is to go with the insurance policy offered directly by the storage facility. This is the path of least resistance—you can sort everything out in one go when you book your unit.

The second route is to use an existing policy, like your home insurance, or find a specialist third-party insurer. This takes a bit more effort on your part but can sometimes give you broader coverage or even save you a few quid, especially if your current home policy has a decent extension clause.

Facility-Provided Insurance: The Convenient Choice

Most storage companies offer their own insurance plans, built specifically to cover items kept in their units. The biggest selling point here is sheer simplicity. You can add the cover straight onto your rental agreement without any fuss, and the premium is usually just tacked onto your monthly storage bill.

These policies are designed to handle the typical risks you'd find in a storage environment—things like fire, floods, theft from a forced entry, or water damage from a burst pipe. And because it's their own product, the claims process can be more straightforward since the staff on-site already know the drill.

Convenience is the key advantage of facility-provided insurance. It eliminates the need to research external providers and ensures your goods are covered from the moment you move them in, with a policy built for the storage environment.

Using Your Home Contents Policy or a Third-Party Insurer

On the flip side, you might be able to extend your existing home contents insurance to cover your stored items. Many policies have an ‘away from home’ clause, but you absolutely have to read the fine print. While it can be a great money-saver, it’s not without its potential traps.

To get your head around the basics, it’s worth reading a comprehensive guide to homeowners insurance policies, as many of the core principles are the same. When you’re looking at your own policy, keep a sharp eye out for these details:

- Single Item Limits: Your policy might have a pretty low cap on the value of any one item covered outside your house.

- Total Value Limits: The total cover for items stored elsewhere is often just a small fraction of your overall policy value.

- Specific Exclusions: Some home policies will flat-out refuse to cover anything kept in a commercial self-storage facility.

If your home policy just isn’t going to cut it, a specialist third-party insurer is another fantastic option. These companies live and breathe storage insurance, so they often offer very competitive rates and specialised cover that’s a perfect fit for what you need.

Comparing Your Storage Insurance Options

So, which way should you go? It all comes down to what you value most—is it speed and convenience, the lowest cost, or the most comprehensive cover for your specific items? To help you figure it out, here’s a quick side-by-side look at how the two main options stack up.

Comparing Your Options Side by Side

Making the right choice comes down to weighing the pros and cons of each path. The best option for you depends on what you value most—be it convenience, cost, or the level of cover required for your specific items. Here's a quick comparison to help you decide.

| Feature | Facility-Provided Insurance | Home Contents Insurance Extension |

|---|---|---|

| Convenience | Very High: Set up instantly at the facility. | Low to Medium: Requires contacting your insurer and checking policy details. |

| Cost | Competitive: Often priced per £1,000 of cover per month. | Variable: May be included, but could increase your overall premium. |

| Coverage Scope | Specific: Tailored for common storage risks. | General: May have limitations or exclusions for storage units. |

| Claims Process | Direct: Facility staff can guide you. | Indirect: You deal solely with your home insurance provider. |

Ultimately, taking a few minutes to compare these points against your own needs will ensure your belongings are properly protected without any nasty surprises down the line.

What Your Policy Actually Covers and Excludes

It’s one thing to have insurance, but it’s another to know exactly what it protects you against. Think of your content insurance for storage not as a vague safety net, but as a list of very specific promises from your insurer.

Each promise covers a particular type of disaster, known in the industry as a ‘peril’. These are the unexpected events you’re paying to be protected from, so it pays to know what they are. While policies can differ between providers, most will shield your belongings from the usual suspects.

What Is Typically Covered

A solid policy is designed to step in when things go wrong. Imagine a pipe bursting in the unit above yours, flooding your belongings and ruining your electronics and furniture. That’s precisely the kind of scenario where your insurance kicks in to cover the replacement costs.

Most standard policies will have your back in case of:

- Fire: If a blaze breaks out in the facility and damages your unit.

- Theft: Covers burglary, though it usually requires clear evidence of a forced entry.

- Flood and Water Damage: Protects against everything from burst pipes and leaky roofs to external flooding.

- Vandalism: If someone breaks into your unit and maliciously damages your things.

- Storms and Natural Disasters: Includes damage from events like heavy winds or lightning strikes.

- Impact: Covers damage caused by something hitting the building, like a vehicle or a falling tree.

It’s worth remembering that policies cover the financial value of your items, not the sentimental value. That’s why having a detailed inventory is so important—it helps ensure you get a fair and accurate payout if you ever need to file a claim.

Common Policy Exclusions

Just as crucial as knowing what’s covered is understanding what isn’t. Every insurance policy has exclusions—specific items or situations the insurer simply won’t pay out for. These aren’t hidden in the small print to catch you out; they’re listed because certain items are too risky or need their own specialist cover.

You can find more details in our complete guide to contents insurance for storage.

Insurers won’t cover items that could cause damage themselves, like flammable liquids or explosive materials. It just makes sense. Here are some of the most common things you’ll find on the exclusion list:

- Certain High-Value Items: Jewellery, fine art, and antiques often have a very low single-item limit. They may even need a separate, specialist policy to be properly covered.

- Cash and Securities: Money, stocks, and bonds are almost never covered. Don’t store them in your unit.

- Living Things: This includes plants, pets, or anything else that’s alive.

- Perishable Goods: Food and other items that can spoil or rot are a no-go.

- Illegal Items: Anything that’s illegal to own or store won’t be covered. Obvious, but important.

- Vehicles: Cars, motorbikes, and boats all require their own dedicated insurance policies.

- Damage from Mould or Vermin: Gradual damage from pests, mildew, or damp usually isn't covered unless it was the direct result of a covered event, like a flood.

The golden rule? Always declare any high-value items to your provider. It’s the only way to be sure they’re properly protected.

How to Accurately Value Your Stored Goods

One of the biggest mistakes you can make with content insurance for storage is guessing what your belongings are worth. It’s an easy trap to fall into; you throw a rough figure together, buy a policy, and figure you’re covered. The problem is, if you ever need to make a claim, you could end up seriously out of pocket.

Getting the valuation right is the most critical step in protecting your stored items. It ensures you’re not overpaying for cover you don’t need, but more importantly, it guarantees you have enough to replace everything if the worst happens. Think of it as creating an honest financial snapshot of everything inside your unit.

This is more important than ever. The UK self-storage industry has exploded, now pulling in over £1.2 billion a year. That number tells a story about just how much valuable stuff is being locked away across the country. You can find more insights on the UK's expanding self storage market at januseurope.com.

New for Old vs Indemnity Cover

Before you start tallying things up, you need to understand how insurers think. Most storage insurance policies are sold on a 'new for old' basis, which is great news for you.

- New for Old: This means if an item is stolen or destroyed, the policy pays out what it would cost to buy a brand-new equivalent today. So, if your five-year-old sofa gets ruined, you’ll get enough cash to go out and buy a new one.

- Indemnity Cover: This is less common for storage insurance. It only pays out the item's current value, factoring in all the wear and tear. That same five-year-old sofa would be valued at a much lower, second-hand price.

Always double-check your policy wording, but assuming it’s ‘new for old’, your job is to figure out the total replacement cost of everything in your unit.

A Simple Guide to Creating Your Inventory

To get an accurate figure, you need to roll up your sleeves and make a detailed list of every single thing going into storage. I know, it sounds tedious, but it's the only way to be sure you have the right cover.

A detailed inventory isn't just for calculating your insurance cover; it's also your most powerful tool if you ever need to make a claim. It provides clear, undeniable proof of ownership and value.

Just follow these simple steps:

- List Everything: Go box by box, or room by room if that’s easier, and jot down every item. A simple spreadsheet or a notes app on your phone works perfectly. For big collections of similar things, like books or vinyl records, you can group them and estimate a bulk replacement cost.

- Take Photographs: A picture is worth a thousand words—and potentially thousands of pounds in a claim. Snap clear photos or take a quick video of your belongings before you pack them away. For high-value items like electronics or designer furniture, get close-ups of serial numbers and brand labels.

- Find Replacement Costs: This is the important part. Hop online and research what it would cost to replace your main items today, brand new. For that TV, check current retail prices for a similar model. For your bed frame, see what an equivalent one costs now.

- Keep Receipts for High-Value Items: If you still have the receipts for expensive things—think electronics, jewellery, or specialist tools—scan them or take a photo. Digital copies saved with your inventory are rock-solid proof of value.

- Add It All Up: Once your list is complete, total up all the replacement costs. This final number is the amount of insurance cover you need to be fully protected.

Navigating the Claims Process with Confidence

Finding out your stored items have been damaged or stolen is a horrible feeling, but knowing what to do next can make a stressful situation much easier to handle. The key to a smooth, fast resolution is understanding your content insurance for storage claims process before you ever need it.

Those first few moments are crucial. As soon as you discover a problem, your first move should be to tell the storage facility manager immediately. This officially logs the incident and lets them secure the area, check for issues affecting other units, and start their own internal process.

After that, your next steps will depend on what happened. Acting quickly and staying organised will make your claim much stronger.

Your Immediate Action Checklist

If you’ve been the victim of a crime, like theft or vandalism, your next call is to the police. They’ll give you a crime reference number, which is a non-negotiable piece of information for your insurance claim. For other events like a fire or water damage, your focus should be on documenting absolutely everything.

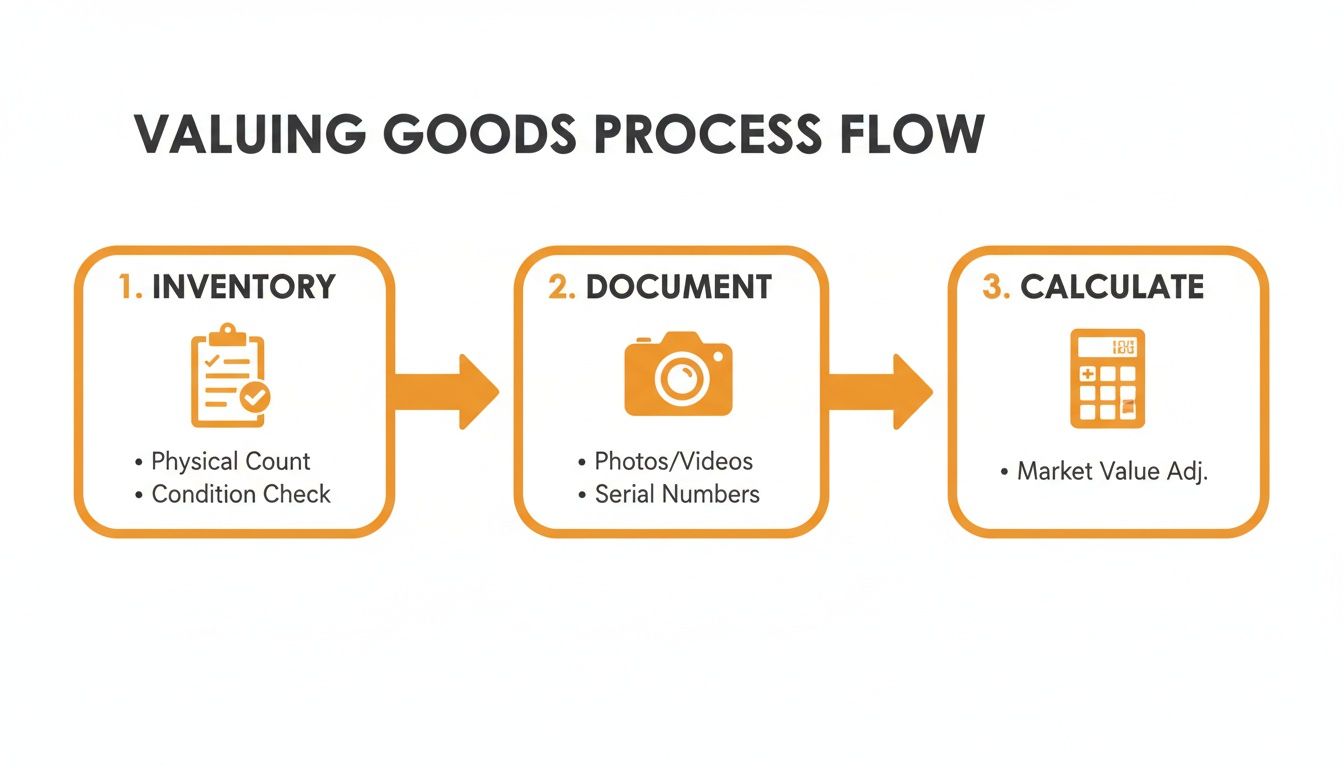

Here’s a simple three-step process for valuing your goods to back up your claim.

This process—inventory, document, and calculate—is the bedrock of a successful claim. With these details ready, it’s time to contact your insurance provider and formally get the ball rolling. They’ll walk you through their specific steps, which usually involve filling out a claim form and submitting all the evidence you’ve gathered.

For business customers, keeping clear records is vital, a practice we cover in our guide on document archiving best practices.

For larger or more complicated claims, your insurer might bring in a loss adjuster. This is an independent expert who assesses the damage and the value of your claim, which is why having your detailed inventory and photos prepared is so important. If you want to get a broader feel for how these things work, this guide on understanding insurance claims is a great resource.

By staying organised and proactive from the start, you can navigate the claims process with confidence and work your way toward a fair outcome.

Tailored Insurance Advice for Every Storage Need

Not everyone uses storage for the same reason, which means a one-size-fits-all approach to content insurance for storage just doesn’t cut it. Your needs will shift dramatically depending on what you're storing and why. Getting the right cover is all about thinking through your unique situation.

A homeowner stashing furniture during a renovation faces completely different risks than a tradesperson storing thousands of pounds worth of power tools. Once you know which category you fall into, you can zero in on the policy features that actually matter, making sure you aren't underinsured or paying for protection you don't need.

For E-commerce Sellers and Small Businesses

For a business, a storage unit isn't just extra space—it's an extension of your warehouse, a mini stockroom. That makes insuring your inventory and equipment a critical financial decision, as standard policies often fall short for commercial goods, especially if you have high-turnover stock.

It’s a bigger deal than you might think. Nearly a quarter of all UK storage users—24% to be exact—run a business from their unit. These spaces often hold inventory worth thousands, a huge investment that demands proper protection. You can dig into more data on the commercial use of UK self-storage at clevelandcontainers.co.uk.

When insuring business stock, always hunt for a policy that specifically covers 'goods for resale'. This makes sure your inventory is valued correctly and protects you against lost profits if the worst happens.

For Homeowners and Renters

If you’re moving house, finally tackling that decluttering project, or renovating, your storage unit is probably packed with personal effects and furniture. The main goal here is simple: straightforward replacement cover. Your priority should be a 'new for old' policy that pays out enough to buy brand-new replacements for any damaged items.

- Create a detailed inventory: Jot down a list of all furniture, electronics, and the general contents of each box.

- Photograph valuable pieces: Snap a few pictures of antiques or designer furniture as proof of their condition.

- Check your home insurance first: Your existing policy might have some 'away from home' cover, but you must verify the limits and exclusions for storage facilities. Don't just assume you're covered.

For Tradespeople and Students

Tradespeople rely on their tools for their livelihood, which makes robust insurance an absolute non-negotiable. When storing tools and equipment, look for policies with high single-item limits to cover expensive, specialised machinery. It's also vital to confirm the policy covers theft from a locked unit, as tools are a magnet for thieves.

For students storing belongings between terms, the game is all about cost-effective, short-term cover. You likely don’t need a massive policy. Just calculate the replacement cost of your books, laptop, and personal bits and pieces to find an affordable plan that gives you essential peace of mind.

A Few Final Questions About Storage Insurance

To wrap things up, here are a few quick answers to the questions we hear most often about content insurance for storage. Getting these points clear will help you lock in your policy with total confidence.

Is Insurance Mandatory for a Storage Unit in the UK?

While it isn't a nationwide legal requirement, you’ll find that pretty much every reputable storage facility will ask for proof of insurance before you sign a rental agreement. It’s a policy that protects both you and them.

You can usually buy a policy directly through the facility for convenience, or you can provide evidence that you’re already covered—often through an add-on to your existing home contents insurance.

How Is the Cost of Storage Insurance Calculated?

It almost always comes down to the total replacement value of your goods. Insurers keep it simple, typically charging a set rate per £1,000 of cover each month.

So, for example, insuring £5,000 worth of belongings might cost you somewhere between £5 and £10 monthly, but this can definitely vary. The only way to know for sure is to get a quote based on a detailed inventory of what you're storing.

Remember, the goal isn't just to find the cheapest price, but to get the right level of cover. Under-insuring to save a few quid could leave you seriously out of pocket if you ever need to make a claim.

Can I Adjust My Coverage Level Later On?

Yes, absolutely. Flexibility is a standard feature on most storage insurance policies.

If you add valuable items to your unit or take a significant amount out, just get in touch with your provider to adjust your cover. This makes sure you’re always correctly insured—never paying for more protection than you need, and never leaving your newest items unprotected.

At Standby Self Storage, we believe in making the process of securing your belongings simple and transparent. From picking the right unit to understanding your insurance options, our team is here to help you every step of the way. Book your secure unit online in minutes.